Institutional ownership increased from 87.4 M shares as of June 13 to 97.6 M shares as of June 30

Institutional ownership increased from 87.4 M shares as of June 13 to 97.6 M shares as of June 30

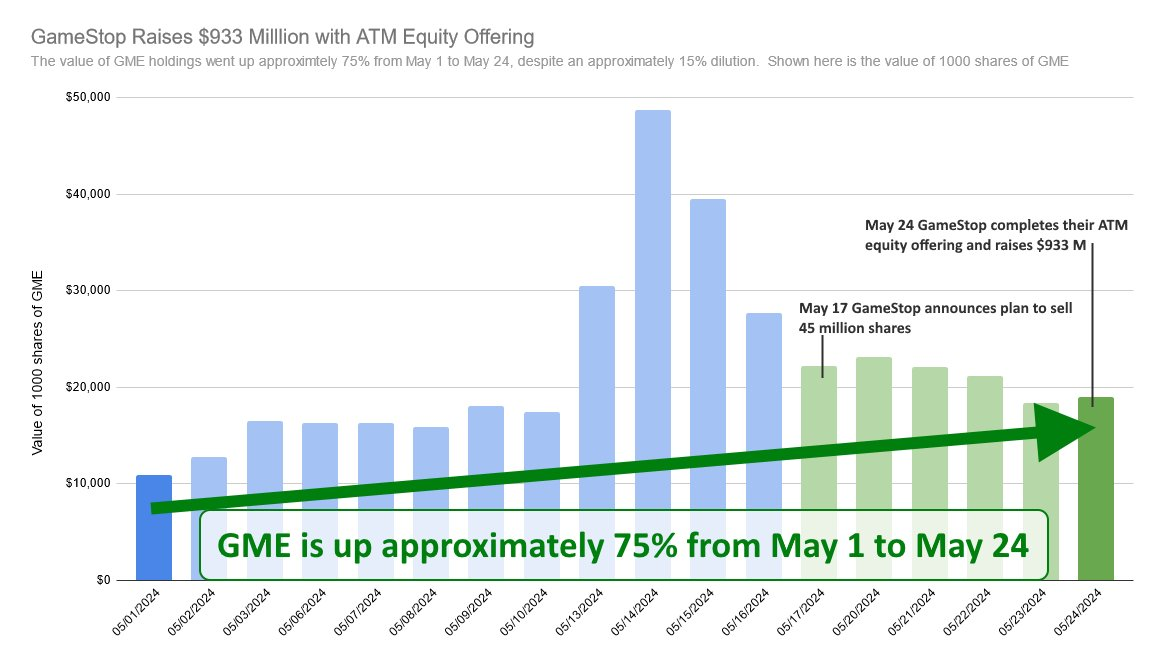

On May 17 GameStop announced plans to sell up to 45 million shares, and on May 24th they announced that all 45 million shares were sold for $933 million, at an average price of about $20.73.

Modifying shares outstanding from 306 million to 351 million is an approximately 15% dilution. A shareholder could have expected the value of their own share holdings to have dropped 15% from this action, but shareholder value hardly went down at all as a consequence of the dilution and in fact is up about 75% from May 1 to May 24.

Reddit as a whole continues to demonstrate corrupt acts of information control against the interest of Reddit's users.

Imagine being a shareholder of any company but not allowed to have a voice in shareholder social media communities because the unaccountable moderators / admins of those communities decided that you don't get a voice. how fucked up is that? this is the power that reddit has over shareholders of companies that have nothing to do with Reddit. it's one of the reasons i have reluctantly found myself using X more. X too suffers from problems but not censorship the way reddit does.

i of course would ultimately love to see more users on Lemmy and other fediverse apps, but most people are not really interested in this right now. maybe as the enshittification of reddit gets unbearable, more people will consider Lemmy

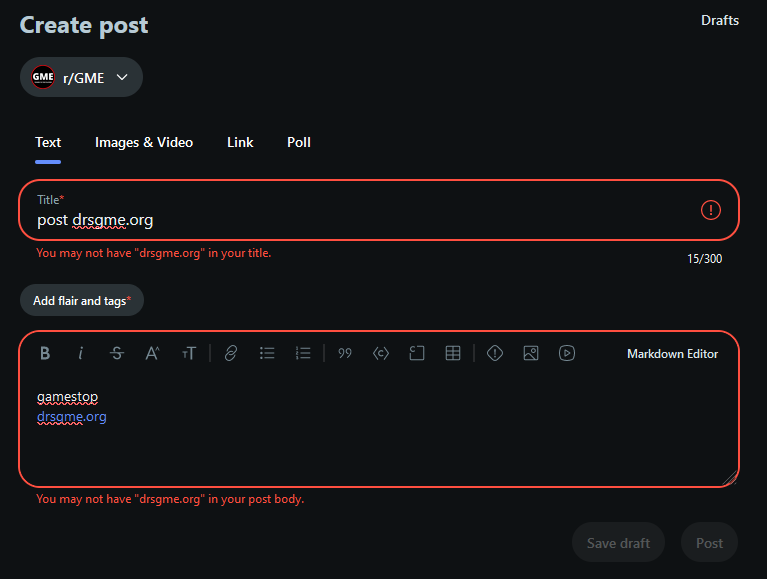

was trying to post something to r/GME and had used a page on the DRSGME.org website as a source.

Specifically, it was the 2023 stockholder list viewing page that I had wanted to use a source because it is a good source. It is pretty much the only source of data that GME shareholders have that provide numbers about DRS versus DSPP. An imperfect, out-of-date set of data, sure, but it's all we've got.

Turns out, r/GME will not allow any linking to DRSGME.org.

Why would that be?

A free information website built by GME shareholders for other GME shareholders and anyone else, is not permitted in the r/GME subreddit. Huh?

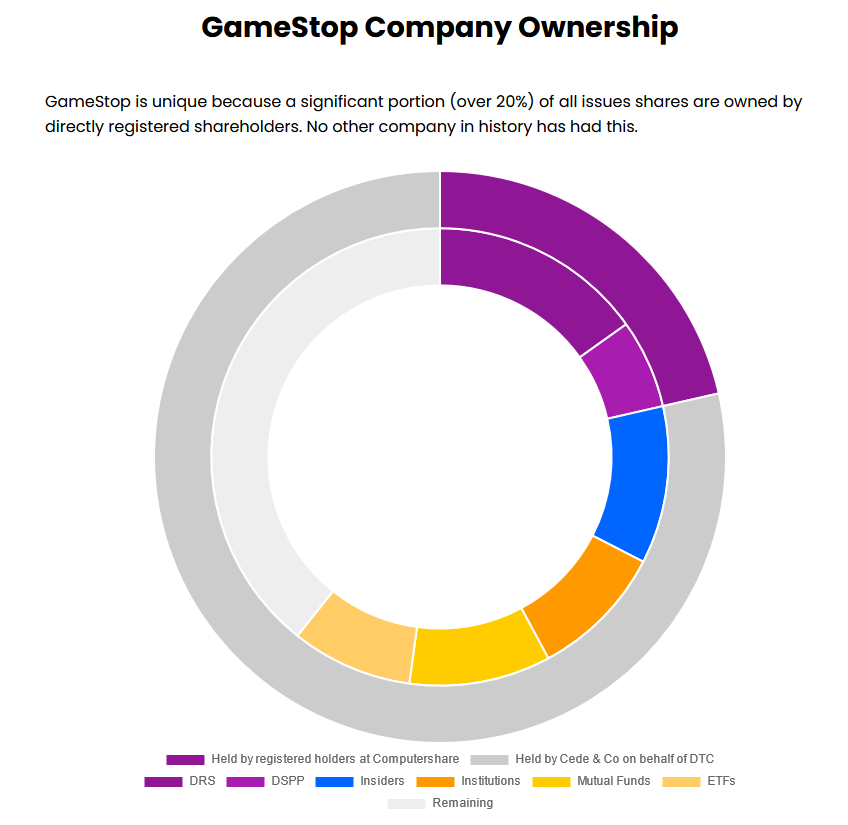

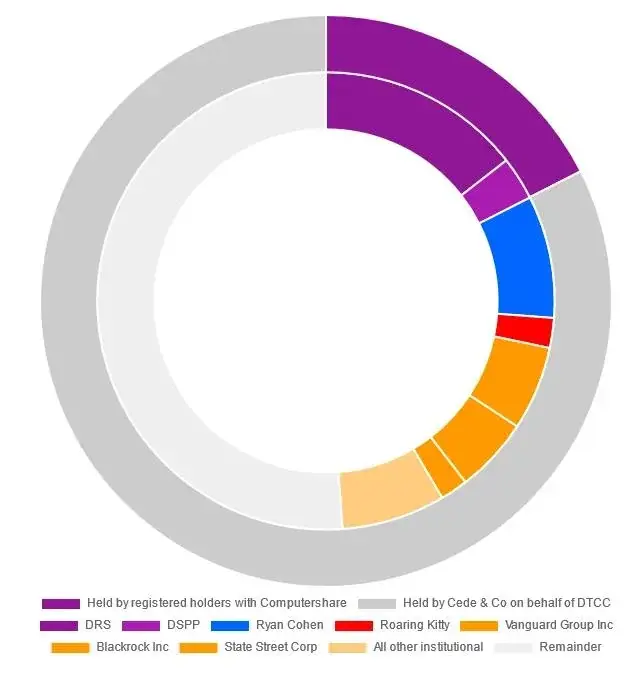

As of March 20, 2024 there were 305,873,200 shares of GameStop's Class A common stock (GME) outstanding.

"Of those outstanding shares, approximately 230.6 million were held by Cede & Co on behalf of the Depository Trust & Clearing Corporation (or approximately 75% of our outstanding shares) and approximately 75.3 million shares of our Class A common stock were held by registered holders with our transfer agent (or approximately 25% of our outstanding shares)."

25% of issued shares of GME are owned by directly registered shareholders

The other 75% is held by Cede & Co on behalf of the DTCC

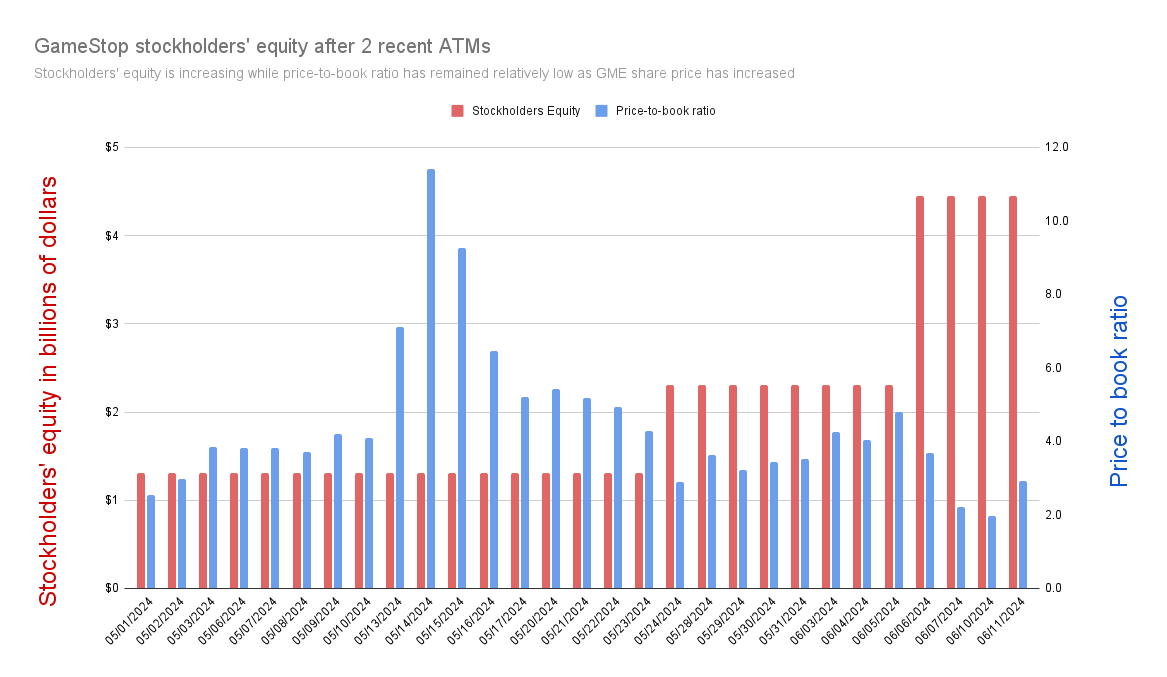

As of May 24, 2024, GameStop completed an at the market equity offering, and sold 45,000,000 shares, increasing the total amount of shares outstanding to approximately 351,000,000.

Information about DRS versus DSPP counts held at Computershare are not reported publicly.

This information is available, however, on the GameStop stockholder list which can be viewed in person at GameStop headquarters.

The latest data we have was from 2023 when GME shareholders viewed the stockholder list and obtained some data including DRS vs DSPP counts. Source: https://www.drsgme.org/2023-stock-list-viewing

The DRS vs DSPP numbers in the graphic have been rounded for simplicity based off the data from that 2023 source.

Of shares held by Computershare: 53 million DRS, 22 million DSPP.

| Before ATM | After ATM (May 24) | |

|---|---|---|

| Shares outstanding (approx) | 305,000,000 | 350,000,000 |

| Cash on hand (approx) | $1 billion | $2 billion |

| DRS % of outstanding shares (approx 75 million DRS) | 24.7% | 21.4% |

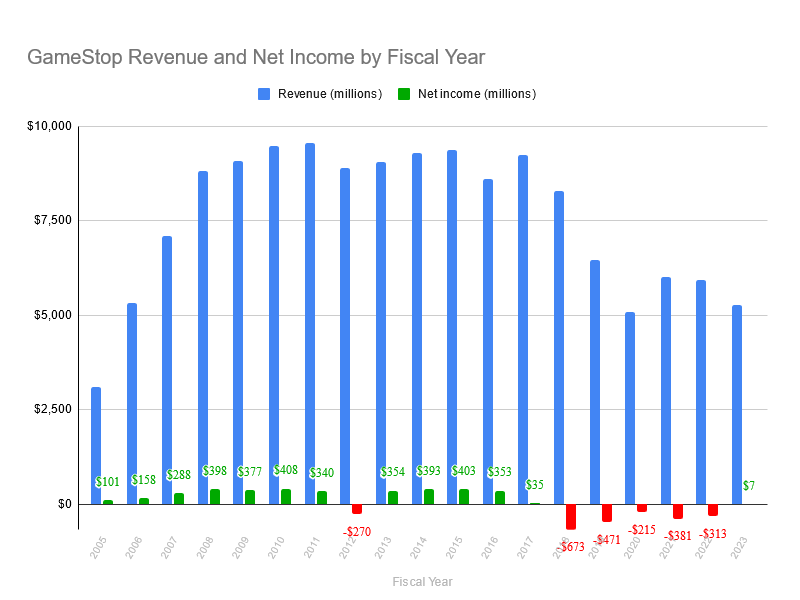

GameStop reported full-year profitability for fiscal year 2023, contradicting the prevailing media sentiment that GameStop is a terrible company destined for bankruptcy

From a historical point of view, GameStop was consistently profitable every fiscal year from 2005 through 2016, with the exception of 2012. Starting in fiscal year 2017, GameStop began showing reduced profitability, and from FY 2018 through FY 2022, was unprofitable.

Source: GameStop 10-K filings - Google Sheets

Looking exclusively at revenue, it is clear that there has been a significant reduction starting approximately with fiscal year 2019. Much of this can be attributed to the fact that gamers are increasingly buying games digitally rather than in the form of physical discs such as can be purchased at a brick-and-mortar retail store like GameStop.

Yet, even in fiscal years 2017 and 2018, it is clear that despite high revenues the company was not performing well.

Heading through 2020, GameStop was undeniably a struggling company facing significant challenges, and according to many was destined for bankruptcy. The trading price of GME reflected this prevailing sentiment, and the financial media was dutifully critical.

In 2020, activist investor Ryan Cohen began purchasing shares of GME, ultimately becoming the largest individual owner of the company with approximately 12% ownership. By June 2021, the entire board of directors of the company was replaced by Ryan Cohen and his associates, with Ryan Cohen becoming chairman of the board. From this time onward, control of the company was completely in the hands of this new leadership team.

"We inherited a bunch of legacy everything, and under-investment across the entire business –- people, the entire technology stack, just decades of neglect, and so it’s hard to turn around a brick and mortar retailer that’s under the kind of pressure that GameStop was and continues to be under, but that was also part of the attraction going into GameStop was that a transformation the likes of GameStop was really unprecedented and I was motivated by that."

The company went from a situation where it was losing hundreds of millions of dollars per year to net profitability in fiscal year 2023.

While this is an undeniably positive result for the company in this time period, GameStop continues to face numerous challenges and must continue to improve and adapt in order to successfully compete in the modern video game industry.

What does mainstream financial media have to say about GameStop achieving full-year profitability for the first time in 6 years?

GameStop faces 'unsustainable' sales decline, cuts jobs to control costs

GameStop Q4 Earnings Highlights: Retail Favorite Stock Plunges After Revenue, EPS Miss

GameStop Stock Plummets Following Q4: Profitability Fails to Offset Significant Revenue Miss

GameStop Stock Plunges After Earnings Fall Short of Expectations—Key Level to Watch

Jim Cramer Says GameStop Is Arguably The Worst Company In America

GameStop could be gone in less than 5 years, says analyst

GameStop Needs To Get Its Game Back

GameStop Confirms More Layoffs, Share Price Tumbles After Sales Slide

A Sales Slump Is the Kiss of Death for GameStop Stock

GameStop saga ends. Winner: capital markets

GameStop Stock: Is This The End of a Saga Or Just Another Chapter?

Searching for recent news about GameStop yields mostly negative sentiment that fails to even mention at all that GameStop achieved full-year profitability for the first time in 6 years.

Failing to mention this important detail is a deliberate decision that reveals a clear bias in the media. It goes beyond just reporting about true negative facts about GameStop. It demonstrates a deliberate effort, by those culpable writers and media outlets, to propagate a specific sentiment about the company that is not allowed to even mention contextually important true positive facts about the company.

GameStop was profitable for the first time in 6 years - this is the news headline that captures the significance of GameStop's recent earnings report. Yet, an unassuming person who consumes mainstream financial media likely would not even learn about this important fact at all.

Who would benefit from that?

Why are there competing, mutually exclusive narratives?

There are competing narratives because there are competing financial interests.

One of the listed news articles, GameStop saga ends. Winner: capital markets, from Reuters, draws some attention to this ongoing conflict while declaring that the conflict is actually over and one side has won and one side has lost.

GME shareholders that believe in the company turnaround and leadership, despite the real challenges faced by GameStop, have a vested financial interest in the success of the company, with a desire for the share price of GME to go up, and naturally will promote the narrative that supports this financial interest.

In opposition to GME shareholders are all of the financial market participants that have a vested financial interest in the share price of GME going down. An example of such a participant would be any hedge fund that has a net short position on GME. The article refers to this faction as "shorts", recogonizing that such a faction with an interest does exist. Naturally, members of this faction will promote the narrative that supports their financial interest.

If the prospect of GameStop's success was not an ongoing threat to one faction of incumbent market participants, then there would be no reason to deliberately omit the fact of GameStop's profitability, to pretend that it isn't something that even happened at all.

Recognizing that there is an ongoing financial competition between factions that stand to benefit financially from a particular outcome of the GME share price, which faction benefits when most mainstream financial media articles propagate negative sentiment about GameStop and deliberately ignore the contextually significant fact that GameStop was profitable?

It is clear: much of mainstream financial media is actively propagating biased narratives to the benefit of the faction that has a vested financial interest in the share price of GME going down.

An interactive version of this article can be found at gmetimeline.org/fy23-profitability

never left, not leaving. will be buying more shares and putting them in my name

thanks for your concern though

it may very well be one of the last good opportunities to get some GME for cheap.

Either GameStop achieves full-year profitability, or they don't.

GameStop's opponents (those hedge funds and other participants holding a short position seeking the stock price to go down), and their useful bought and paid for media puppets, are well aware of the situation we are in, probably even more aware than most GME shareholders.

Full-year profitability is the target. It's the thing that most shareholders and opponents have their mind on, in terms of material things that matter that could change the narrative, change the dynamic, and ultimately lead towards true price discovery.

If GameStop fails to achieve full year profitability, (e.g. net quarterly earnings for 2023 Q4 to be any amount less than positive ~ $57 million), then this will give the opponents an opportunity to pile on negative sentiment and hit the price down. "After 3 years in control of the company, Ryan Cohen and team fail to achieve widely-expected profitability, stock price down XX %". As a shareholder I obviously hope that this is not the outcome, but I'll be happy with any general improvements to the company's financial standing.

but I think that this is a very achievable target. Net positive $57 million for 2023 Q4 will give full-year profitability for FY 2023. Any number above that is a major success, and completely feasible. Not guaranteed by any means, but realistically achievable.

And if this is achieved, then it shoots a giant hole in the persistent negative media narrative that has been put upon GameStop these past few years by dishonest and manipulative wall street incumbents and their dishonest and manipulative friends in the financial media.

in the scenario of full-year profitability, some positives with respect to an investment in GME:

Obviously, not everything is sunshine and rainbows. GameStop still faces headwinds and has many competitors. In the long term, GameStop also needs to dramatically grow top-line revenue if it ever wants to become the giant that many shareholders believe it to be. These are not small accomplishments.

In the short term, in the face of the achievement of full-year profitability, and all the other positives that GameStop has going for it, how can the media sentiment towards GameStop continue to be so negative and cynical? Surely they will try, but it will become increasingly untenable to try and spin negativity about a situation that is very obviously positive. The negative media narrative is there to try and prevent additional investors from ever considering GME as a valid investment. But at some point the truth of the fundamentals become more powerful than the lies of the media. All it will take is some significant buying pressure and the price could break out.

Who knows what will happen.

I hope GameStop reports $57 million or more in net earnings for Q4 2023. We'll find out in less than 2 weeks.

i disagree with the assertion that heat lamp has been debunked, though it seems like some people really want people to necessarily believe this to be true and final.

put aside the name "heatlamp theory" and address 2 of the main points:

Okay, so heat lamp as originally proposed might not be the fully accurate explanation for the volume spikes. So what are the alternative explanations then?

Something worth noting is that there seems to be a very effortful push to authoritatively declare "DEBUNKED!" without explaining specifically how it is debunked, and without providing any alternative explanations.

Plan is not DRS is a true statement and is not debunked.

GME has unusual trading volume on some DRS record dates, this is another true observation that is not debunked.

One theory that attempts to tie these things together might not be completely accurate but to my awareness is the most thoughtful explanation that exists thus far. I'd love to see alternative explanations but I don't know of any. Superstonk mods by consensus are opposed to the notion that there is any validity to heatlamp theory, yet offer absolutely nothing else as an alternative.

TLDR: "heatlamp is debunked" is just another example of narrative control being perpetrated by a group of moderators of the largest GME internet community. More information is needed to make any kinds of authoritative claims.

exciting!

with respect to GME, filing date for Q4 is usually mid March

| Quarter | Filing Date | Document Date |

|---|---|---|

| Q4 2022 | March 21, 2023 | January 28, 2023 |

| Q4 2021 | March 17, 2022 | January 29, 2022 |

| Q4 2020 | March 23, 2021 | January 30, 2021 |

| Q4 2019 | March 26, 2020 | February 1, 2020 |

| Q4 2018 | April 2, 2019 | February 2, 2019 |

Updated image, original image was missing Technology Brands stores for FY 2013.

The link is in the post, they are all on that page, but here:

As a reminder, shareholder proposals are submitted by real people with real names. As a matter of courtesy it would be appropriate to respect the privacy of these individuals as much as possible.

And to my awareness, it does not matter which country a shareholder resides in, the qualifications to submit a proposal are only that a shareholder has held a minimum dollar value of shares for a minimum amount of time, as specified here:

some more data going back to fiscal year 2005.

| Fiscal Year | Revenue | Net Income | Store Count | Revenue Per Store | Net Income Per Store | 10-K |

|---|---|---|---|---|---|---|

| 2005 | $3,091,783,000 | $100,784,000 | 4490 | $688,593.10 | $22,446.33 | link |

| 2006 | $5,318,900,000 | $158,250,000 | 4778 | $1,113,206.36 | $33,120.55 | link |

| 2007 | $7,093,962,000 | $288,291,000 | 5264 | $1,347,637.16 | $54,766.53 | link |

| 2008 | $8,805,897,000 | $398,282,000 | 6207 | $1,418,704.20 | $64,166.59 | link |

| 2009 | $9,077,997,000 | $377,265,000 | 6450 | $1,407,441.40 | $58,490.70 | link |

| 2010 | $9,473,700,000 | $408,000,000 | 6670 | $1,420,344.83 | $61,169.42 | link |

| 2011 | $9,550,500,000 | $339,900,000 | 6683 | $1,429,073.77 | $50,860.39 | link |

| 2012 | $8,886,700,000 | -$269,700,000 | 6602 | $1,346,061.80 | $40,851.26 | link |

| 2013 | $9,039,500,000 | $354,200,000 | 6675 | $1,354,232.21 | $53,063.67 | link |

| 2014 | $9,296,000,000 | $393,100,000 | 6690 | $1,389,536.62 | $58,759.34 | link |

| 2015 | $9,363,800,000 | $402,800,000 | 7117 | $1,315,694.82 | $56,596.88 | link |

| 2016 | $8,607,900,000 | $353,200,000 | 7535 | $1,142,388.85 | $46,874.59 | link |

| 2017 | $9,224,600,000 | $34,700,000 | 7276 | $1,267,811.98 | $4,769.10 | link |

| 2018 | $8,285,300,000 | -$673,000,000 | 5830 | $1,421,149.23 | $115,437.39 | link |

| 2019 | $6,466,000,000 | -$470,900,000 | 5509 | $1,173,715.74 | $85,478.31 | link |

| 2020 | $5,089,800,000 | -$215,300,000 | 4816 | $1,056,852.16 | $44,705.15 | link |

| 2021 | $6,010,700,000 | -$381,300,000 | 4573 | $1,314,388.80 | $83,380.71 | link |

| 2022 | $5,927,200,000 | -$313,100,000 | 4413 | $1,343,122.59 | $70,949.47 | link |

🤷

🫡